Which is Best: Cash Back or Points?

Neither flexible rewards credit cards nor cash back is perfect. They are just suitable for different situations and uses. Hence, before choosing a service provider, you must know what bonuses are best for you.

While using rewards credit cards, you get additional points for every purchase or target action made; with cash back cards, you receive a specific percentage of money spent back to your account.

This way, rewards are more popular among airline and hotel partners or travel companies. They are also available in apps designed specifically to treat users with a unique rewards program.

Through such apps, people access an extensive network of merchants to earn bonuses for every purchase and spend them with maximum return on investment. On the other hand, cash back is more universal. It enables consumers to return a part of their spending by purchasing from any store that offers cash back.

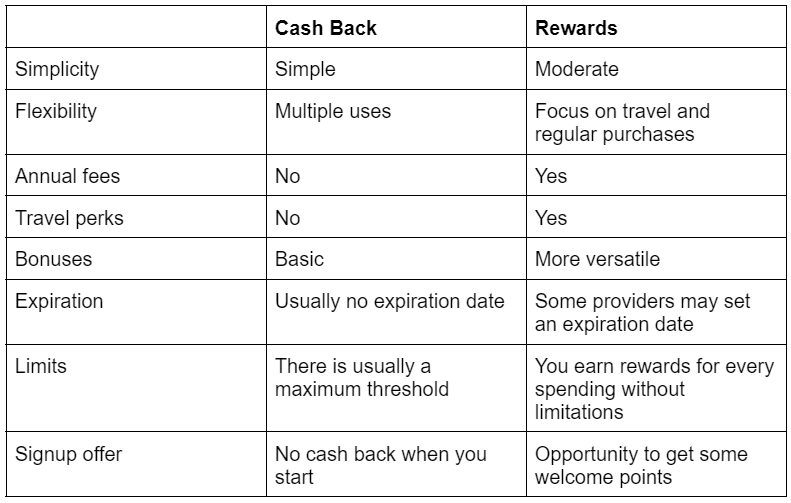

Here’s a brief comparison that should help you make up your mind:

As you see, rewards cards are more sophisticated. They offer more advanced bonuses while charging annual fees. Cash back credit cards have no annual fees but limit the amount you can save and offer no signup bonuses.

Let’s discuss both options in more detail below.

What is a Cash Back Credit Card?

Cash back credit cards are similar to regular credit cards, but they allow you to get a part of the money you spend back. You can choose a category of purchases you’d like to earn bonuses for or buy from merchants partnering with a card issuer. The issuer usually provides detailed information on its partners and their cash back percentage. You can check it on the official website of the financial services provider or download their apps with a listing.

The ways to get money back vary depending on the card. A flat-rate card has the same rate for every purchase. There is no difference whether you pay at a restaurant or order a book online. With other cards, you may enjoy higher rates for certain types of payments. For example, earning cash for utility bills or groceries may be the most advantageous.

You may also come across cards that change percentages for different categories of goods and services from time to time. In this case, you may benefit from seasonal offers and earn exceptionally high bonuses if you buy something at the right time.

How Does It Work?

While a rewards credit card generates bonuses, cash back cards actually provide you with money. You may receive a check from the card issuer, transfer funds to your bank account, or pay with cash back at online platforms like Amazon.

The exact functionality, limits, and charges depend on a provider and the types of cards. So if you want a cash back card, you need to pick the preferred provider, examine their rates, and send them a request with up-to-date information to receive a card.

Here are the main cash back card types and how they work:

Flat-rate

Flat-rate cards offer the same percentage for all qualifying purchases. You may earn a percentage for every purchase, be it a new gadget or groceries.

For many years, a 1% cash-back reward rate was an industry standard followed by all providers. Yet, as the competition in the credit card industry is getting fiercer, 1.5% and even 2% rates become more common.

In particular, you may enjoy unlimited 1.5% cash back on all purchases made with Capital One Quicksilver Cash Rewards Credit Card, American Express Cash Magnet® Card, or Chase Freedom Unlimited®. If you want a 2% cash back rate and up, you can get it by opening a Wells Fargo Active Cash® Card or Citi® Double Cash Card, etc.

Tiered-rate

Tiered-rate cards allow users to return more money for specific categories of purchases. These are usually dining, groceries, gas (check out the best ways to earn cash back on gas here), or travel-related transactions. Besides higher cash back rates in selected categories, some tiered-rate cards also support a low flat rate (usually 1%) for other purchases.

Each provider offers its own higher rate categories. Thus, you must know your spending patterns to get more value from a tired-rate credit card. The spending habits will help you choose the most suitable provider.

For example, Savor Rewards from Capital One offers unlimited 4% money back on entertainment & streaming services and 3% at grocery stores. A cash rewards card by the Bank of America allows cardholders to choose one of the eligible categories for a 3% cash back and offers 2% at groceries and wholesale clubs.

Rotating-category

This type of credit card is for those who chase ultimate rewards. You can find rotating-category cards with 5% cash back or even more. So, what’s the deal?

The killer rewards are available only for specific categories of spending, which regularly change. As a rule, the card issuer rotates the cash-back areas every three months, and you need to adapt to it. Hence, such rewards cards are suitable mainly for people ready to change their spending patterns based on what the card issuer dictates.

Discover it® Cash Back and Chase Freedom Flex are the most well-known rotating-category cards. So if you like this option, these are the issuers you may consider.